A reaffirmation in bankruptcy means agreeing to the original terms of a loan agreement after filing for Chapter 7 bankruptcy. This post is about what these reaffirmation agreements are and how they work in a bankruptcy case.

We highly recommend speaking with your bankruptcy attorney before signing such an agreement.

Call Stone Rose Law at (480) 739-2448 to speak with our experienced Phoenix bankruptcy attorney and get a free consultation.

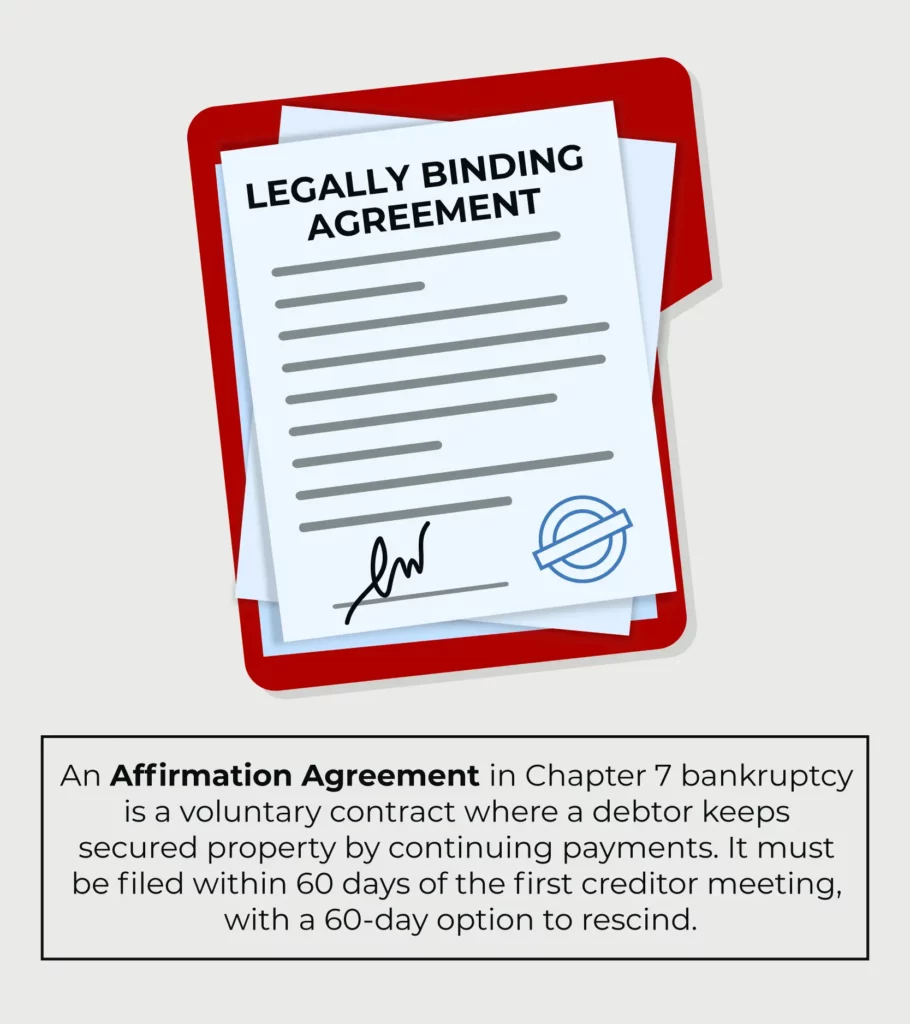

A reaffirmation agreement is a strictly voluntary agreement between a Chapter 7 bankruptcy debtor and a creditor that, for practical purposes, takes an item of personal property subject to secured financing outside of bankruptcy.

What you are reaffirming in the agreement is that you will remain liable for your debt obligation.

This means that when your bankruptcy is closed, and your other debts are discharged, the reaffirmed debt will remain. You can keep possession of the property if you keep your payments current under the new agreement.

Reaffirmation agreements are used mainly with secured debts, meaning financing that puts a lien on the property as collateral. Unsecured debts, like credit card balances, personal loan payments, and medical bills, are examples of unsecured debt and are usually not subject to reaffirmation agreements but discharged under Chapter 7 with no remaining personal liability on your part.

A reaffirmation agreement is not always a continuation of the terms of your original financing contract with a lender, although it often amounts to that. Under the reaffirmation agreement, you may have the opportunity to renegotiate your payment amounts and rate of interest on the loan, but the lender is under no obligation to offer you better terms.

You must enter into a reaffirmation agreement within 60 days after your first meeting with creditors, although the bankruptcy court can extend this period at its discretion.

You or the lender must file the agreement with the bankruptcy court. Once you sign the agreement, you have 60 days to change your mind and back out of it.

Chapter 7 bankruptcy discharge will eliminate many secured and unsecured debts on personal property. For property subject to secured financing (meaning that the creditor has a lien on the property), like an auto loan, bankruptcy discharge eliminates what you owe but does not remove the lien.

This means that if you do not satisfy your discharged payment obligation after bankruptcy, the creditor can still repossess the property under the lien, although it cannot pursue you for the debt.

Here are some circumstances when exploring the possibility of reaffirming a debt may be practical.

You cannot compel a lender to enter into a reaffirmation agreement. But sometimes, allowing you to keep possession of the property under more favorable loan terms may be more in a creditor’s interest than repossession. Some lenders will negotiate lower payments, interest rates, and even principal balance.

You do not always need a reaffirmation agreement to keep property subject to financing. If you seek to keep possession of personal property subject to a creditor’s lien after bankruptcy, you can still make payments to the lender. In this case, however, if you do not reaffirm the debt, the lender is not obligated to report your payments to credit agencies.

Sometimes, the lender will encourage you to enter into a reaffirmation agreement because, by doing so, the agreement and your on-time payments will be reported to credit bureaus, thereby helping you rebuild your credit.

Reaffirmation agreements are not always to your advantage, even when they are an option.

For example, reaffirming a debt neutralizes the advantages of discharging a debt. If you fail to keep up with your payment obligations under the agreement, the creditor can take action against you for breach of contract and seek remedies like repossession or wage garnishment. You cannot resort to bankruptcy protection again.

Also, a reaffirmation agreement is not always necessary to rebuild your credit because there are other ways to accomplish this.

Before you enter into a reaffirmation agreement, you should be sure that you really need or want to hold onto the item of property, no other option exists to keep it from being liquidated or repossessed, and you can reasonably expect to be able to pay off the balance of the loan.

Another consideration is how much equity you have in the property. For example, if the property is worth considerably more than what you owe on it, then a reaffirmation agreement may be worthwhile. However, if the amount you owe is more than what it would cost to replace the item, it may be better to let it go.

An experienced bankruptcy attorney can help you to decide when it is in your best interest to enter into a reaffirmation agreement and when it may not be.

Even if the lender is willing to enter into one with you, a reaffirmation agreement is not always an option. Here are some potential roadblocks to being able to use a reaffirmation agreement.

Many creditors will not consider a reaffirmation agreement if you are already behind on payments with your present financing agreement.

You must obtain court approval for the reaffirmation agreement.

If you have a bankruptcy lawyer representing you, then the lawyer will use an official form to make this attestation to the court. If you do not have a lawyer, then the bankruptcy court will review the agreement to determine if it will cause undue hardship to you. The judge will examine whether, after your basic monthly expenses are met, you still have enough money to make regular payments under the reaffirmation agreement.

Also, if you owe considerably more under the reaffirmation agreement than what the property is worth, the judge can reject the agreement as not being in your best interest.

At Stone Rose Law, our Arizona bankruptcy lawyers represent debtors who need to use the legal process to protect their important assets and keep their belongings when filing bankruptcy. Our law firm provides customized bankruptcy debt relief solutions tailored to your needs.

If you have any questions about whether a reaffirmation agreement is right for you or how the reaffirmation process works, contact us today or call our office at (480) 739-2448.