Neither Arizona law nor the United States Bankruptcy Code requires married couples to file bankruptcy together when one spouse’s financial situation reaches the point where filing bankruptcy becomes a consideration. You can file for bankruptcy individually.

Often, spouses’ finances are intertwined, which can complicate the decision of whether to file individually or jointly. Arizona is a community property state, which can make this decision even more complex.

Stone Rose Law helps Arizona residents who are dealing with overwhelming debt to weigh their debt relief options, including bankruptcy. In this blog post, we specifically cover the considerations that go into whether you can file for Chapter 13 bankruptcy without your spouse.

To learn more about how federal bankruptcy law works in Arizona, and to speak with an Arizona bankruptcy attorney in a free consultation, call Stone Rose Law at (480) 739-2448 or contact us online.

Compared to Chapter 7 “liquidation” bankruptcy, Chapter 13 is commonly called “reorganization” bankruptcy.

Two key differences between these bankruptcy types are that in Chapter 13, you can save some of your property and assets from being sold by the bankruptcy trustee to repay creditors, and that Chapter 13 takes considerably longer to complete. Compared to Chapter 7 bankruptcy, which usually takes four to six months from filing the petition to final discharge, a Chapter 13 debt-repayment plan takes three to five years to complete.

Other key considerations in choosing Chapter 13 bankruptcy include whether you have a stable income to make consistent payments under the payment plan and whether your debts do not exceed the debt limits for Chapter 13. A bankruptcy attorney can help you determine if you meet these requirements.

Fundamentally, community property law means that most assets or debts you or your spouse acquire after you get married become joint assets and obligations. A few exceptions to this general rule exist, like inheritances or gifts made specifically to one spouse. But both of you will be equally responsible for most of the property and debts that either of you acquires or incurs. This includes your home mortgage or trust deed, your car loan, credit card debts, furniture, and more.

Most community property becomes part of the bankruptcy estate when you file for Chapter 13 bankruptcy. Filing a bankruptcy petition without your spouse does not affect keeping marital assets out of the bankruptcy estate. What this means is that if you want to protect a marital asset with a bankruptcy exemption, any non‑exempt equity in community property must be accounted for in the Chapter 13 plan.

Separate assets and debts, usually originating from before you were married, remain separate. So, for example, if you file by yourself but you and your spouse own a house, a car, or joint bank accounts, your individual exemption must protect the community equity in these assets, and any non-exempt portion will increase your plan payment.

For most, it can be advantageous to file for bankruptcy with your spouse. You can combine your debts into one debt repayment plan, and you share one bankruptcy filing fee and one set of attorney fees.

The monthly Chapter 13 plan payment is based heavily on household income and expenses. While a spouse may not be a party, they are contributing to the monthly payments. If there are community debts, the spouse should benefit from bankruptcy protection and credit recovery.

Filing Chapter 13 jointly may also be better if you are both looking for financial recovery. Your credit recovery begins the moment you file, not at the end of your bankruptcy. Most individuals have a credit score of 720 within 2 years of filing for bankruptcy. Both spouses can qualify for credit immediately after filing and even purchase a home while in active bankruptcy.

Here are some situations when filing jointly for Chapter 13 may be more to your advantage:

Many factors go into the decision to file individually and to leave your spouse out of a Chapter 13 bankruptcy case. Here are some questions you will want to consider with your bankruptcy lawyer:

We will examine some of the more important of these considerations below.

If you owe debts jointly with your spouse, but you choose to file separately for Chapter 13, here are some of the possible effects:

When you file separately for Chapter 13, the amount of disposable income you have can have a bearing on whether the bankruptcy court will consider your household income and not just your separate income in determining your debt repayment plan.

This consideration can affect the amount of your payments under your repayment plan, its duration, and the amount your unsecured creditors receive through the plan.

Generally, when you file, your spouse’s credit rating should remain unaffected. Your individual Chapter 13 filing will only appear on your credit report and should not appear on your spouse’s.

However, there are a few cases, such as when joint debts you have included in your debt repayment plan are in delinquency or when your spouse is a co-signer on any of your debts, which can affect your spouse’s credit report.

Also, if you and your spouse seek credit after your bankruptcy filing, future lenders can still consider your separate bankruptcy when evaluating your joint application, so this can have an indirect effect on your spouse’s creditworthiness. This often occurs with home mortgage lenders and car loans.

Arizona is an “opt out” state for bankruptcy exemptions, meaning that if you file in this state, you must use the exemptions provided under Arizona’s Revised Statutes instead of the U.S. Bankruptcy Code.

Arizona law provides for many kinds of possible exemptions. In a Chapter 13 bankruptcy, compared to a Chapter 7 bankruptcy, exemptions do not affect whether the bankruptcy trustee can liquidate assets. Consequently, you keep your property under Chapter 13.

Instead, the effect of exemptions in Chapter 13 is on:

An important thing to keep in mind about exemptions in a Chapter 13 is that the effect of non-exempt equity (the amount of equity you have in property after you apply your exemption) affects your payment amount for your debt repayment plan.

The general rule is that the more non-exempt equity you have, the higher your monthly payment will need to be.

Arizona’s homestead exemption protects equity in your primary residence. It does not automatically double if you and your spouse file for bankruptcy jointly.

Under Arizona law, both spouses can apply their exemptions, even if only one spouse is filing.

If you acquire them during the marriage, cash and savings are community property. If you file Chapter 13 bankruptcy separately from your spouse, your joint exemption will cover all community cash.

A non‑filing spouse’s separate property is generally not included in the bankruptcy estate and does not need to be exempted. If your spouse owns a considerable amount of separate assets, this is a strong consideration in favor of filing separately instead of jointly. There are many factors in determining if an asset is sole and separate or community. It is recommended to consult with an Attorney to identify these assets.

The table below summarizes how filing separately can affect your exemptions compared to filing jointly with your spouse.

| Issue | Individual Filing | Joint Filing |

|---|---|---|

| Community property | Must be exempted by you | You and your spouse can both apply for exemptions |

| Homestead protection | Limited | Often stronger |

| Vehicles & cash | Tighter coverage | More flexibility |

| Separate property | The non-filing spouse’s property is protected | Both spouses’ property is included in the bankruptcy estate |

| Plan payment impact | Often higher | Often lower |

| Bankruptcy trustee scrutiny | Higher | Lower |

Every person’s financial issues and debt situation are unique, so there is no one right answer to the question of what kind of bankruptcy is right for you (Chapter 7 or Chapter 13), or whether you should file together with your spouse or by yourself, or in some cases, whether an alternative to filing for bankruptcy is the best choice.

A Stone Rose Law Arizona experienced bankruptcy attorney can help you assess your debts and advise you on your legal debt relief options and how they can affect your financial future. In a Chapter 13 case, we can help you consider:

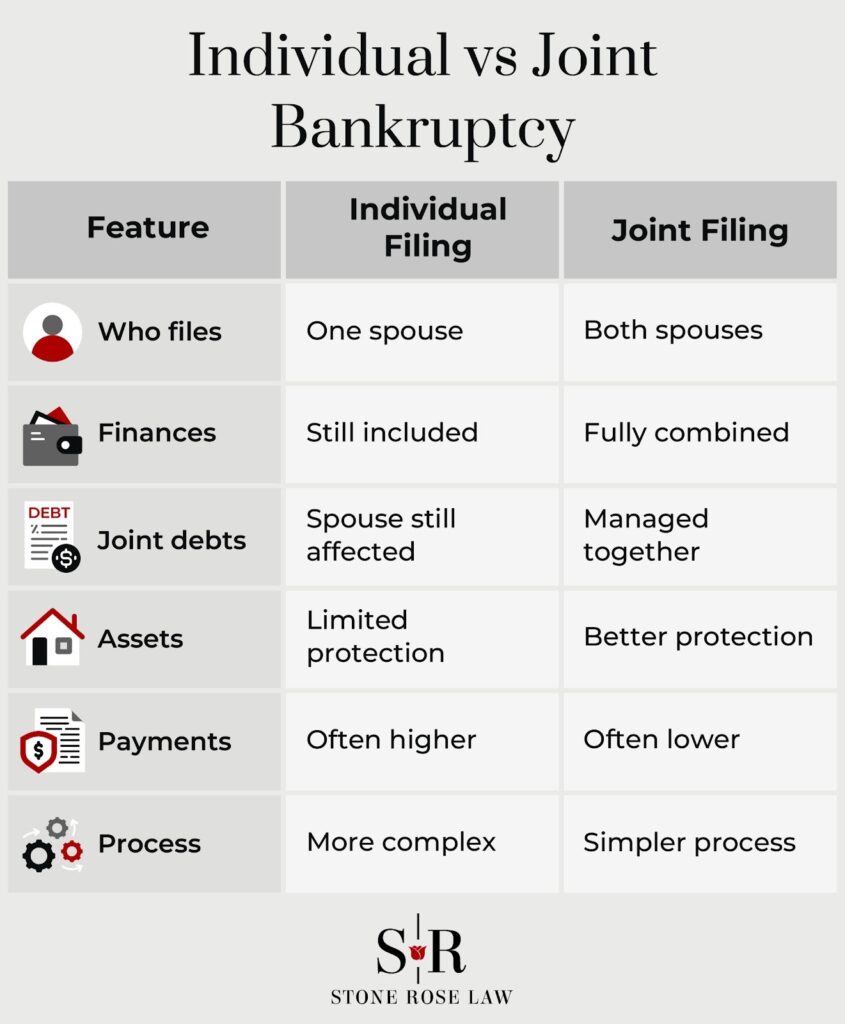

For quick reference, below we provide a side‑by‑side comparison of individual and joint Chapter 13 filings in Arizona, which shows the effects of Arizona’s community property law and Chapter 13 repayment rules.

This table is not exhaustive, but it can give you a starting point for consideration.

| Issue | Individual Chapter 13 (Bankruptcy Without Your Spouse) | Joint Chapter 13 (Both Spouses File) |

|---|---|---|

| Who is the debtor | Only one spouse is legally a debtor | Both spouses are debtors |

| Community property | All community property is still part of the bankruptcy estate, even though only one spouse files | All community property is part of the estate (same result) |

| Separate property | Filing spouse’s separate property is included; non‑filing spouse’s separate property is generally excluded | Each spouse’s separate property is included |

| Household income | Non‑filing spouse’s income must be disclosed and usually counted (subject to marital adjustment) | Both spouses’ incomes are fully counted |

| Plan payment amount | Often similar to a joint case because household income is still used | Often similar, but sometimes clearer and simpler to justify |

| Joint debts | Plan must address them; creditors may still pursue the non‑filing spouse if protections end or plan fails | Joint debts are fully controlled within the plan |

| Co‑debtor protection | Temporary co‑debtor stay may protect non‑filing spouse on consumer debts | No need for co‑debtor stay—both spouses are protected |

| Credit reports | Bankruptcy appears only on the filing spouse’s credit, but joint accounts may still be affected | Bankruptcy appears on both spouses’ credit reports |

| Attorney & filing costs | Slightly lower than joint filing | Slightly higher, but often not double |

| Administrative complexity | More complex (marital adjustment, co‑debtor issues, fairness scrutiny) | Usually more straightforward |

To schedule a free consultation with a Stone Rose Law bankruptcy lawyer, call our law offices at (480) 739-2448. You can call us any time, any day. Or, use our online contact form to reach us.